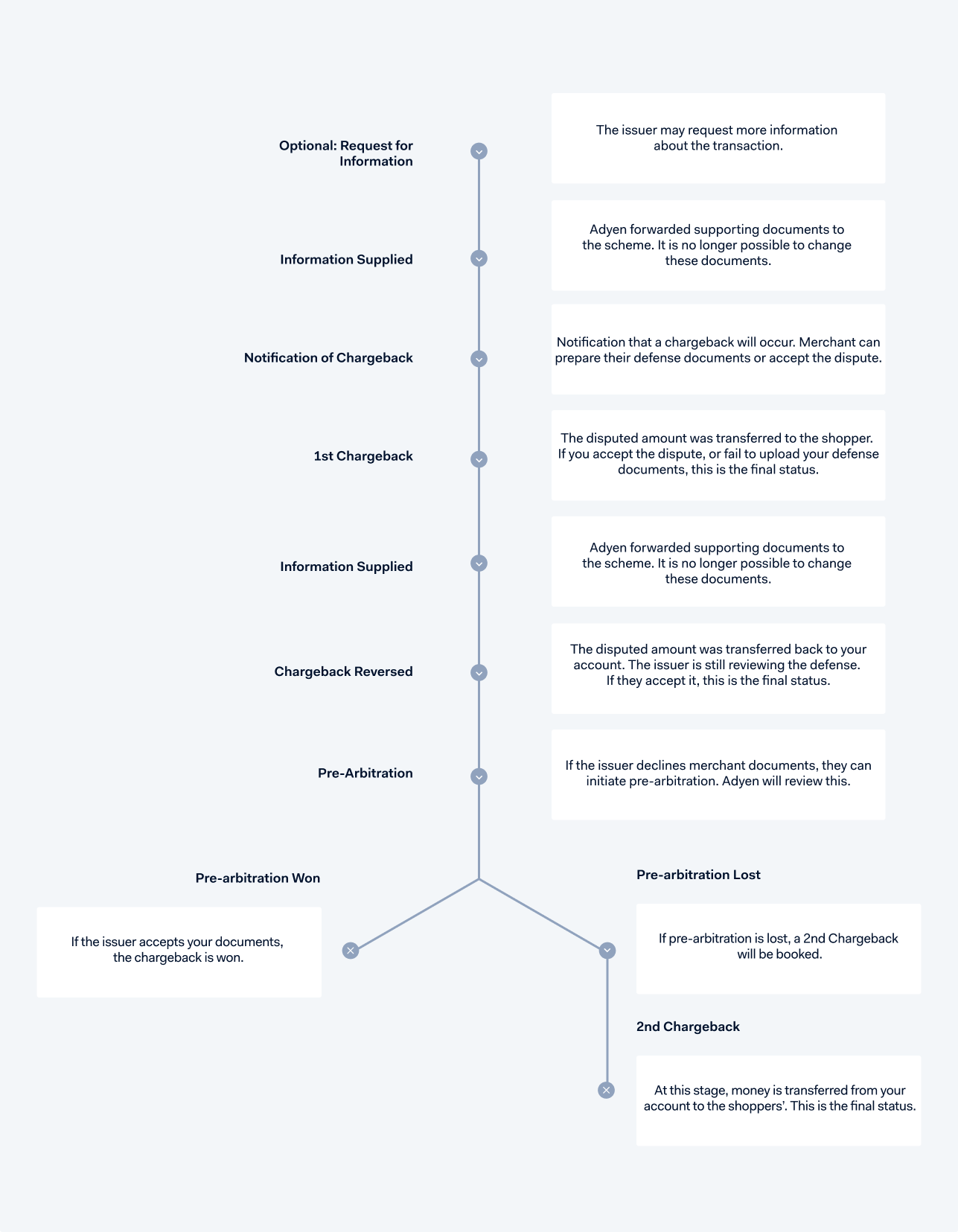

The chargeback flow for Elo cards consists of the following steps:

- Optional: Request for Information

- Information Supplied

- Notification of Chargeback

- 1st Chargeback

- Information Supplied

- Chargeback Reversed

- Pre-Arbitration

- 2nd Chargeback

- Arbitration Case Filing

Elo flow

Optional: Request for Information (RFI)

A Request For Information (RFI) is initiated when the cardholder does not recognize or does not agree to a charge, and requests more information from their bank. It can also be initiated in the context of a fraud investigation where the real cardholder does not acknowledge the transaction.

For an RFI, always upload information that can help the cardholder to recognize the charge or that can support your position that the transaction is valid.

At this point, funds are not yet deducted from your account.

Elo transaction receipt RFI reasons

| Code | Message |

| 01 | Request for copy related to the transaction |

| 03 | Cardholder request for copy related to the transaction due to dispute |

| 04 | Fraud analysis request |

| 05 | Good faith investigation. |

RFI defense recommendations

Code 04: Fraud analysis request: Block the delivery of the goods, if possible, and block the shopper from performing any future payments for fraudulent cases.

Other codes: Upload information that may help the cardholder to recognize the charge or that can support your position that the transaction is valid. Upload information within 18 days.

For physical goods

- Order confirmation/copy invoice.

- Proof that goods are delivered (DHL/UPS signed proof of delivery).

For digital goods

- Order confirmation/copy invoice.

- Proof that services are downloaded/used (date and time of download, IP address, and email address that was used for the download).

Information Supplied

Adyen received your defense documents and forwarded them to the scheme. It is no longer possible to change these documents. The InformationSupplied journal is booked and we send you an INFORMATION_SUPPLIED webhook.

Notification of Chargeback

The issuing bank initiated a Notification of Chargeback (NoC). The NoC can follow from a Request for Information (RFI), or the RFI step is skipped and the NoC occurs immediately after the payment status is set to Settled or Refunded. We send you a NOTIFICATION_OF_CHARGEBACK webhook. The dispute process has started, and money will be withdrawn from your account.

The chargeback debit usually occurs a few days after you receive the NoC.

1st Chargeback

The issuing bank initiates the first chargeback on behalf of the cardholder by sending a chargeback notification to Adyen stating the dispute reason.

We assign the dispute to you for review in your Customer Area > Revenue & risk > Disputes. The NotificationOfChargeback and Chargeback journals are booked, and we send you a CHARGEBACK webhook. At the same time, your account is debited for the chargeback amount.

After your review, you can decide to either:

- Accept the chargeback in your Customer Area or using the Disputes API. The case will be closed for defense.

-

Defend the dispute. You need to upload the relevant defense documents in your Customer Area or using the Disputes API.

See Defense requirements for file formats and for defense documents per dispute type. Be sure to address the dispute reason and provide information that supports your position. An overview of the order details is not enough.You must provide your defense documents within 18 days. There is no opportunity later in the process to provide information or to update information you provided.

Information Supplied

Adyen received your defense documents and forwarded them to the scheme. It is no longer possible to change these documents. The InformationSupplied journal is booked and we send you an INFORMATION_SUPPLIED webhook.

Chargeback Reversed

For Elo chargebacks (Consumer disputes and Processing errors categories), the disputed amount is returned after upload of the defense material.

The Chargeback reversed journal is booked.

Pre-arbitration

The cardholder can challenge your evidence and their bank will send a Pre-arbitration (second chargeback) to Adyen within 30 days of upload date (Information Supplied date).

Pre-arbitration chargebacks are initiated by the bank only for the Elo workflow (Consumer disputes and Processing errors).

In most cases, the cardholder insists that the chargeback is valid (after reviewing your evidence) and requests their bank to continue the dispute.

The Adyen Chargeback Team reviews the Pre-arbitration chargebacks and responds by either accepting or declining them.

If Adyen accepts the case, you will be debited for the disputed amount and a SecondChargeback journal will be booked.

If the Pre-arbitration is declined, the bank can pursue it to the final stage of the dispute cycle by escalating it with Elo.

This is called Arbitration case filing.

2nd Chargeback

If the issuer declines your defense, or Adyen accepts their pre-arbitration case, a second chargeback occurs. You can not upload defense documents. This is the final status.

Arbitration case filing

At Arbitration case filing stage, the Elo chargeback committee will:

- Review the chargeback and provide a ruling.

- Review the cardholder's claim and your documents.

- Compare them with the Elo regulations.

The party that did not meet the dispute conditions and requirements will lose the chargeback and will be held liable for a filing fee of USD 500 (the fee is charged on top of the dispute amount).

Adyen is not responsible if the card scheme rules in favor of the cardholder.

Reason codes and guidelines

For a list of Elo dispute reason codes, see Dispute reason codes.