A dispute goes through a number of stages after it is raised by a shopper. Before you defend a dispute, it is important to understand how the dispute process works.

Dispute process

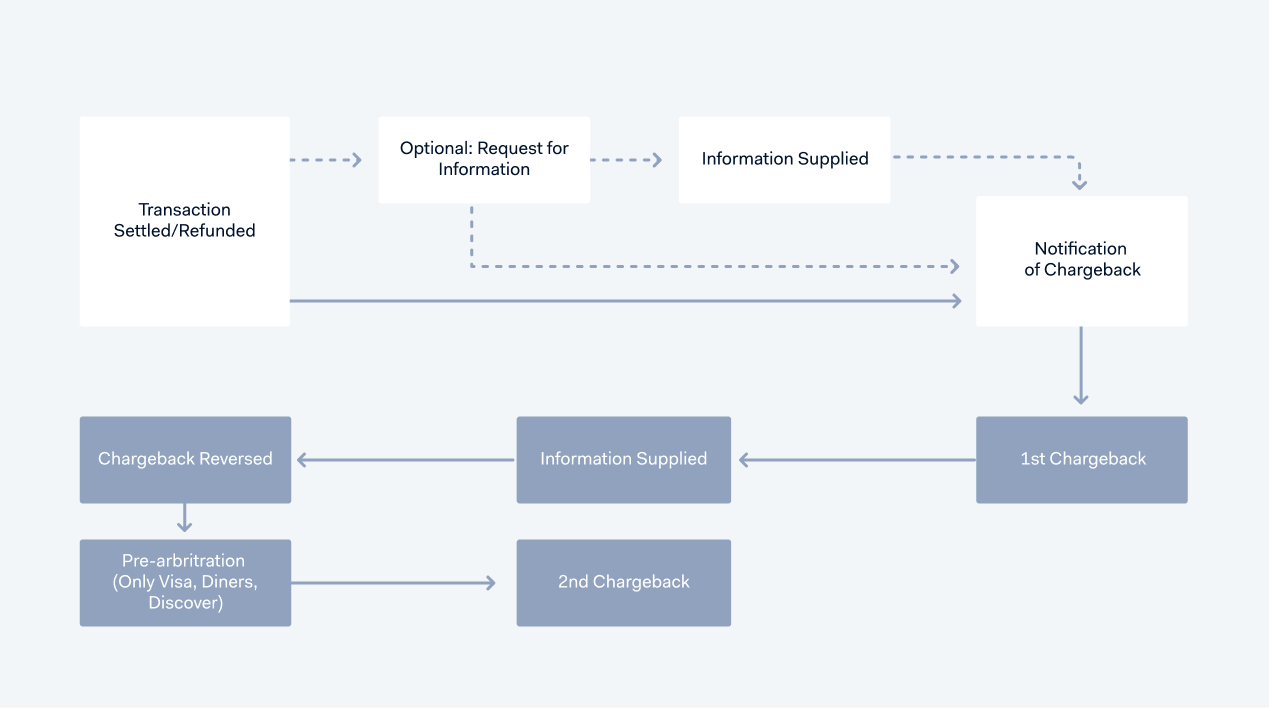

The process can begin with:

-

Optional: Notification of Fraud (NOF) - To notify you of fraud activity, Adyen sends equivalent of a Visa TC40 and Mastercard SAFE (System to Avoid Fraud Effectively) report. This is not a dispute, and no money is withdrawn from your account. This transaction can become a chargeback if there is no 3D Secure liability shift.

Suggested actions:- Actively review the NOF and proactively issue refunds (to avoid a chargeback).

- Block the shopper.

- Stop the shipment of goods if possible.

-

Optional: Request for Information (RFI) - The issuer requests more information about the transaction. At this stage, no money is withdrawn from your account. However, if you do not respond to the RFI in a timely manner, a chargeback may take place, and money may be withdrawn from your account.

Suggested actions:- Provide the requested transactional information to the issuer.

-

Notification of Chargeback (NoC) - A chargeback has been initiated by the issuer, and can be defended. The NoC may follow a RFI, or occur immediately after the payment status is set to Settled or Refunded, skipping the RFI step. The chargeback debit usually occurs a few days after you receive the NoC.

Adyen will automatically defend chargebacks that don't require action on your part, for example fraud chargebacks for which there was a liability shift. To defend a chargeback that can't be automatically defended, you need to upload your defense documents. You can do this either in your Customer Area, or by using the Disputes API.

From there, the dispute continues through the following stages:

- 1st Chargeback - The disputed amount is withdrawn from your account. If you accept the dispute, or fail to upload your defense documents, this is the final stage.

- InformationSupplied - Adyen receives the supporting documents and forwards them to the scheme. It is no longer possible to change these documents.

- ChargebackReversed - The disputed amount is transferred back to your account. In this stage, the issuer reviews the defense. If they accept the defense, or the issuer response timeframe expires, this is the final stage.

- Pre-arbitration (Only Visa, Mastercard, Diners) - If the issuer declines your defense, they open pre-arbitration, which Adyen will review.

- 2nd Chargeback - If the issuer declines your defense, or Adyen accepts their pre-arbitration case, a second chargeback occurs. You can not upload defense documents. This is the final stage.

General flow

The following diagram illustrates the flow of a dispute: