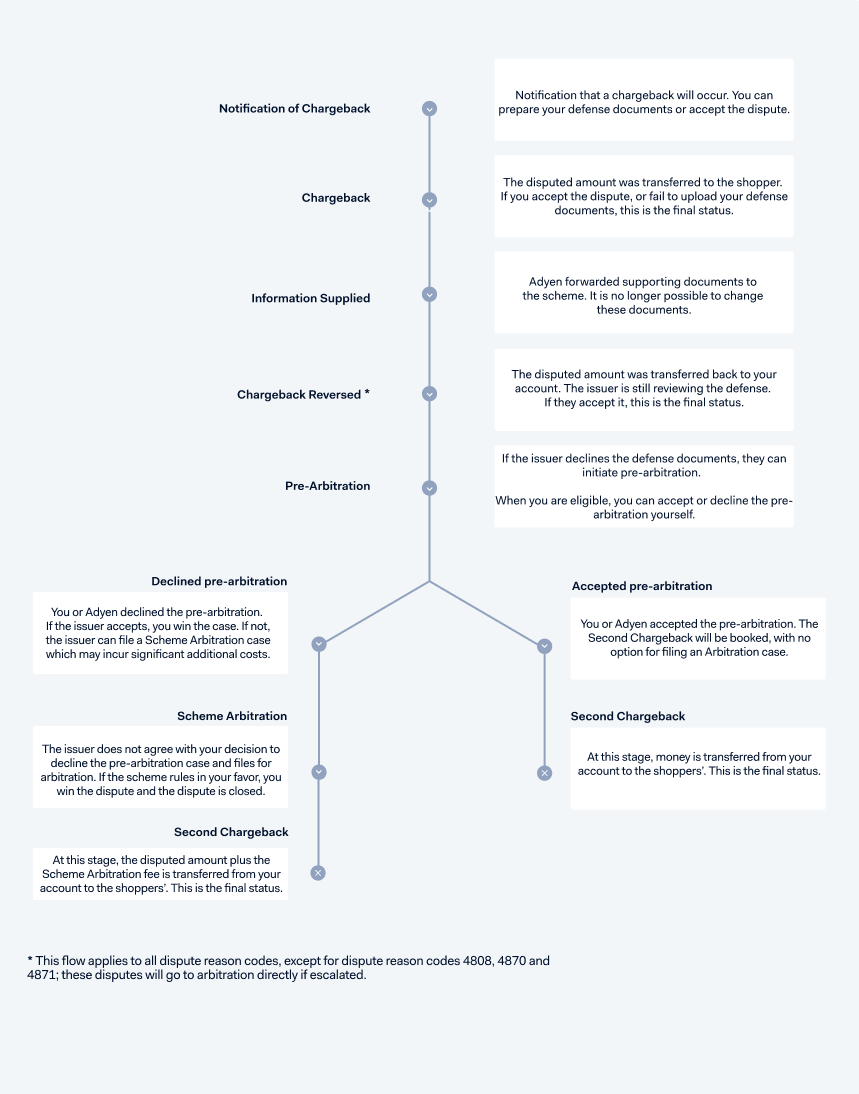

In the Mastercard chargeback process, an issuer can escalate a dispute and file a Pre-Arbitration case. This applies to all Mastercard reason codes, except 4808, 4870, and 4871. These disputes will go to Scheme Arbitration directly if escalated.

The Mastercard chargeback flow:

- Notification of Chargeback

- Chargeback

- Information Supplied

- Chargeback Reversed

- Pre-Arbitration

- Second Chargeback

- Scheme Arbitration

Mastercard flow

Notification of Chargeback

The issuing bank initiated a Notification of Chargeback (NoC). The NoC can occur immediately after the payment status changes to Settled or Refunded. We send you a NOTIFICATION_OF_CHARGEBACK webhook. The dispute process has started, and money will be withdrawn from your account.

The chargeback debit usually occurs a few days after you receive the NoC.

Chargeback

The issuing bank initiates the first chargeback on behalf of the cardholder by sending a chargeback notification to Adyen stating the dispute reason.

We assign the dispute to you for review in your Customer Area > Risk & disputes > Disputes. The NotificationOfChargeback and Chargeback journals are booked, and we send you a CHARGEBACK webhook. At the same time, your account is debited for the chargeback amount.

After your review, you can decide to either:

- Accept the chargeback in your Customer Area or using the Disputes API. The case will be closed for defense.

-

Defend the dispute. You need to upload the relevant defense documents in your Customer Area or using the Disputes API.

See Defense requirements for file formats and for defense documents per dispute type. Be sure to address the dispute reason and provide information that supports your position. An overview of the order details is not enough.You must provide your defense documents within 40 days. There is no opportunity later in the process to provide information or to update information you provided.

There is no opportunity later in the process to provide information, unless this information was not available before.

Therefore, address the dispute reason code and upload information that can support your position. Only uploading an overview of the order details is not enough. Refer to the list of Mastercard dispute reason codes.

Submitting the defense documents is irreversible. The documents are automatically sent back to the issuing bank, through the credit card network.

Information Supplied

Adyen received your defense documents and forwarded them to the scheme. It is no longer possible to change these documents. The InformationSupplied journal is booked and we send you an INFORMATION_SUPPLIED webhook.

Chargeback Reversed

The journal Chargeback reversed is booked and the disputed amount is transferred back into your account. The issuer is still reviewing the defense. If they accept, this is the final status.

If they do not accept, disputes with reason codes 4808, 4870, or 4871 go straight to Scheme Arbitration.

Pre-Arbitration

If the issuer does not find the defense compelling enough, they escalate the dispute by filing a Pre-Arbitration case within 45 days of the date that the defense was uploaded (the Information Supplied date). Pre-Arbitration applies to all reason codes, except 4808, 4870, and 4871. These disputes go to Scheme Arbitration directly if escalated by the issuer.

The Pre-Arbitration case is accepted when the response time expires. You can request our Support Team to decline the Pre-Arbitration case on your behalf, which can lead to significant additional costs if the case is sent to Scheme Arbitration.

When you are eligible, you can accept or decline the Pre-Arbitration case yourself. This requires additional configuration and approval from Adyen. Reach out to our Support Team or your Adyen contact for more details.

If the case is accepted, the dispute is lost, and you receive a second chargeback.

If the case is declined, it can be sent to Scheme Arbitration. We recommend that you only decline if you are confident that the chargeback is not valid, or if you can provide an explanation to refute the issuer's reasoning for sending the pre-arbitration request. If you decline, make sure that the defense materials provided during the first chargeback defense were sufficient.

Second Chargeback

If you or Adyen accept the issuer's Pre-Arbitration case, a second chargeback occurs. You cannot upload defense documents. This is the final status.

Scheme Arbitration

If you or Adyen decline the Pre-Arbitration and the issuer accepts the declined case, the case is won. If the issuer does not agree, they have the option to file a Scheme Arbitration case. This means the dispute is escalated to the card scheme.

Also, escalated disputes with reason codes 4808, 4870, or 4871 go straight to Scheme Arbitration.

During Scheme Arbitration, Mastercard rules on the chargeback liability based on the information provided throughout chargeback defense timelines. If Mastercard rules in favor of the issuer, you can incur a fee of up to USD 600. This fee is added to the Second Chargeback. The Scheme Arbitration process can take several months to complete.

Adyen is not responsible if the card scheme rules in favor of the cardholder.

Reason codes and guidelines

For dispute reason codes and defense requirements, see: