Visa disputes are routed in two default workflows, called Allocation and Collaboration. The differences between the flows are:

- The Allocation flow relates to all fraud and authorization cases.

- The Collaboration flow relates to all consumer disputes and processing errors.

There is another process called the Visa Rapid Dispute Resolution (RDR) workflow. This process is separate from and cannot be combined with the default chargeback workflows.

The RDR flow is handled by Verifi, a company that Visa acquired. It automates the dispute resolution process based on conditions that you set. When you use the RDR flow, you can resolve a customer claim via a refund instead of a chargeback, before it becomes a dispute.

Overview

The Visa Allocation flow:

The Visa Collaboration flow:

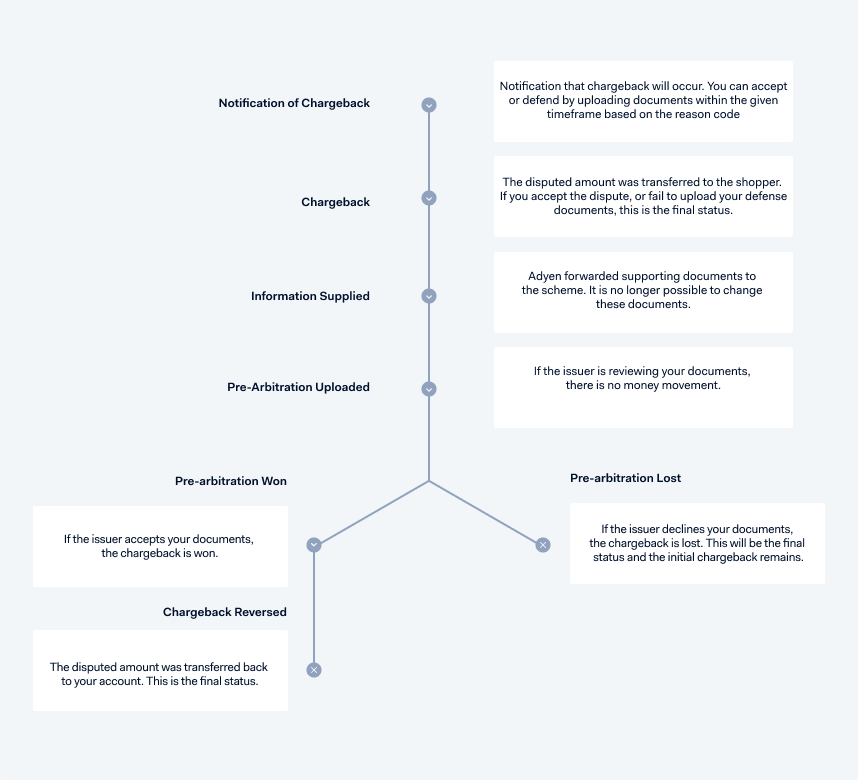

Visa Allocation Flow

Notification of Chargeback

The issuing bank initiated a Notification of Chargeback (NoC). The NoC can occur immediately after the payment status changes to Settled or Refunded. We send you a NOTIFICATION_OF_CHARGEBACK webhook. The dispute process has started, and money will be withdrawn from your account.

The chargeback debit usually occurs a few days after you receive the NoC.

Chargeback

The issuing bank initiates the first chargeback on behalf of the cardholder by sending a chargeback notification to Adyen stating the dispute reason.

We assign the dispute to you for review in your Customer Area > Risk & disputes > Disputes. The NotificationOfChargeback and Chargeback journals are booked, and we send you a CHARGEBACK webhook. At the same time, your account is debited for the chargeback amount.

After your review, you can decide to either:

- Accept the chargeback in your Customer Area or using the Disputes API. The case will be closed for defense.

-

Defend the dispute. You need to upload the relevant defense documents in your Customer Area or using the Disputes API.

See Defense requirements for file formats and for defense documents per dispute type. Be sure to address the dispute reason and provide information that supports your position. An overview of the order details is not enough.You must provide your defense documents within 9 or 18 days. There is no opportunity later in the process to provide information or to update information you provided.

From 21 July 2025, the response timeframe for disputes opened on payments processed locally in the United States and Canada is 9 days. For disputes opened before this date in the United States or Canada, and for all other countries and regions, the response timeframe is 18 days.

Without 3D Secure Liability shift, it is difficult to challenge the dispute. Defense documents should only be supplied if all requirements have been met.

For Allocation chargebacks, if you defend the dispute, the chargeback amount will not be immediately transferred back.

Information Supplied

Adyen received your defense documents and forwarded them to the scheme. It is no longer possible to change these documents. The InformationSupplied journal is booked and we send you an INFORMATION_SUPPLIED webhook.

Pre-arbitration

In line with Visa's dispute flow called Visa Claims Resolution (VCR), Adyen will automatically create a Pre-Arbitration case (containing your documents) and forward it to the bank. The bank has 30 days to review the documents and can respond by accepting or declining the case.

If the Pre-Arbitration is accepted by the bank, we book a Pre-Arbitration won and Chargeback reversed. This is the final stage.

If the Pre-Arbitration is declined, you will be informed with the Pre-Arbitration lost dispute status. The status of the dispute will remain as chargeback.

If you do not agree with the Pre-Arbitration lost dispute status, due to a valid reason, such as the following:

- When the transaction had 3D Secure liability shift, and the chargeback was issued with a fraud reason code.

- When the transaction had already been fully refunded.

In these cases, contact the Adyen Disputes Team within 5 days of the Pre-Arbitration lost dispute status.

Adyen is not responsible if the card scheme rules in favor of the cardholder.

Chargeback Reversed

The Pre-Arbitration has been won, the disputed amount was transferred to your account. This is the final status.

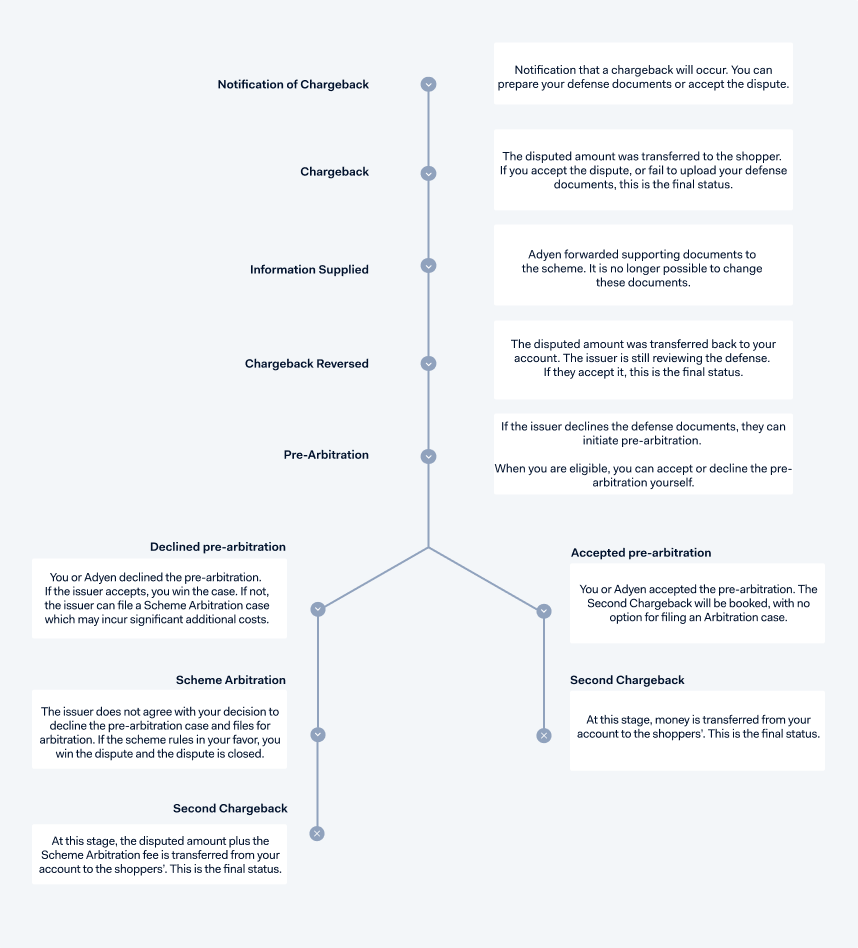

Visa Collaboration flow

Notification of Chargeback

The issuing bank initiated a Notification of Chargeback (NoC). The NoC can occur immediately after the payment status changes to Settled or Refunded. We send you a NOTIFICATION_OF_CHARGEBACK webhook. The dispute process has started, and money will be withdrawn from your account.

The chargeback debit usually occurs a few days after you receive the NoC.

Chargeback

The issuing bank initiates the first chargeback on behalf of the cardholder by sending a chargeback notification to Adyen stating the dispute reason.

We assign the dispute to you for review in your Customer Area > Risk & disputes > Disputes. The NotificationOfChargeback and Chargeback journals are booked, and we send you a CHARGEBACK webhook. At the same time, your account is debited for the chargeback amount.

After your review, you can decide to either:

- Accept the chargeback in your Customer Area or using the Disputes API. The case will be closed for defense.

-

Defend the dispute. You need to upload the relevant defense documents in your Customer Area or using the Disputes API.

See Defense requirements for file formats and for defense documents per dispute type. Be sure to address the dispute reason and provide information that supports your position. An overview of the order details is not enough.You must provide your defense documents within 9 or 18 days. There is no opportunity later in the process to provide information or to update information you provided.

From 21 July 2025, the response timeframe for disputes opened on payments processed locally in the United States and Canada is 9 days. For disputes opened before this date in the United States or Canada, and for all other countries and regions, the response timeframe is 18 days.

Information Supplied

Adyen received your defense documents and forwarded them to the scheme. It is no longer possible to change these documents. The InformationSupplied journal is booked and we send you an INFORMATION_SUPPLIED webhook.

Chargeback Reversed

For Collaboration chargebacks (Consumer disputes and Processing errors categories), the disputed amount is returned after upload of the defense material.

The Chargeback reversed journal is booked.

Pre-arbitration

The cardholder can challenge your evidence and their bank can send a Pre-arbitration (second chargeback) to Adyen within 30-32 days of the upload date (Information Supplied date).

Pre-arbitration chargebacks are initiated by the bank only for the Collaboration workflow (Consumer disputes and Processing errors).

In most cases, the cardholder insists that the chargeback is valid (after reviewing your evidence) and requests their bank to continue the dispute.

The Pre-Arbitration case is accepted when the response time expires. You can request our Support Team to decline the Pre-Arbitration case on your behalf, which can lead to significant additional costs if the case is sent to Scheme Arbitration.

When you are eligible, you can accept or decline the Pre-Arbitration case yourself. This requires additional configuration and approval from Adyen. Reach out to our Support Team or your Adyen contact for more details.

If the case is accepted, the dispute is lost, and you receive a second chargeback.

If the case is declined, it can be sent to Scheme Arbitration. We recommend that you only decline if you are confident that the chargeback is not valid, or if you can provide an explanation to refute the issuer's reasoning for sending the pre-arbitration request. If you decline, make sure that the defense materials provided during the first chargeback defense were sufficient.

Second Chargeback

If the issuer declines your defense, or you or Adyen accept their pre-arbitration case, a second chargeback occurs. You cannot upload defense documents. This is the final status.

Scheme Arbitration

At the Scheme Arbitration stage, the Visa chargeback committee reviews the chargeback and provides a ruling. They review the cardholder's claim and your documents, and compare them with the Visa regulations. The party that did not meet the dispute conditions and requirements will lose the chargeback and will be held liable for a filing fee of USD 600. This fee is charged on top of the dispute amount.

Adyen is not responsible if the card scheme rules in favor of the cardholder.

Visa Rapid Dispute Resolution flow

Verify offers you the option to decide if a transaction is an RDR or a default chargeback. When you use the RDR flow, you have the option to create rules to decide if a disputed transaction should go through the RDR flow, or the default chargeback flow. When a dispute is rapidly resolved, it is resolved through a refund and does not become a chargeback.

Differences between a regular chargeback and an RDR chargeback

Although an RDR is a refund, in Adyen, RDR qualified transactions are referred to as chargebacks. However, there are some differences between a regular chargeback and an RDR. They are:

- The RDR flow relates to all customer claims that are resolved through a refund before becoming a chargeback.

- The RDR process is handled by Verifi.

- You cannot defend an RDR chargeback because a transaction qualifies as an RDR only when it follows certain rules and parameters, and is resolved before becoming a dispute.

- You will not be charged any chargeback or interchange fees for transactions that go through the RDR flow, and these transactions are not included in the dispute count.

How to see an RDR chargeback

If you are processing an RDR chargeback, you can see the chargeback:

- In your Customer Area.

- You can see an RDR indicator field in the Dispute details for each Visa dispute. It will show Yes or No. To see the RDR indicator:

- Log in to your Customer Area.

- Select a merchant account.

- Go to Risk & disputes > Disputes.

- Under Payment methods, select Visa.

- Select a Dispute PSP reference. In the Dispute details section, you can see whether the dispute was processed through RDR.

- You can see an RDR indicator field in the Dispute details for each Visa dispute. It will show Yes or No. To see the RDR indicator:

- In the dispute transaction details report.

- To be able to see the RDR column, follow the steps to add the RDR specific column to the report before you generate it.

- In dispute webhooks.

- This applies only if you manage disputes using the Disputes API, and have configured dispute webhooks.

- After you enable the RDR indicator field, the field

rapidDisputeResolutionwill be included in theadditionalDataobject for CHARGEBACK and NOTIFICATION_OF_CHARGEBACK webhooks. To enable the RDR indicator field:- Log in to your Customer Area.

- Go to Developers > Webhooks.

- Next to Standard webhook, select the edit webhook icon .

- Under Additional Settings > Revenue & risk, select the edit icon .

- Enable Add Visa Rapid Dispute Resolution (RDR) indicator to dispute events.

- Select Apply.

Reason codes and guidelines

For dispute reason codes and defense requirements, see: